The Missing Middle in Parametric Insurance

Hidden opportunities for market expansion in the climate insurance market

Parametric Insurance and Basis Risk

Climate change poses unprecedented challenges, and addressing its impact on communities and industries requires innovative solutions. One promising avenue is parametric insurance, offering climate insurance that is more affordable and scalable than traditional solutions. However, parametric insurance faces a critical obstacle: the pervasiveness of basis risk.

Parametric solutions provide a promising way to bridge this protection gap, by cutting off the costs of taking insurance to markets. Based on a predefined trigger, payouts are activated whenever a parameter (rainfall, for instance) hits a threshold value, as established by an independent third party (like a satellite or an official weather station). It is a simple and efficient solution. However, pure parametric solutions suffer from basis risk.

Basis risk is the difference in the potential risk that arises from mismatches in a hedged position. Basis risk occurs when a hedge is imperfect, so that losses in an investment are not exactly offset by the hedge. Therefore, basis risk manifests when the climate event takes place and the end user experiences damages, but the insurance does not compensate for the losses. This affects the user experience and may ultimately jeopardize the sustainability of the insurance product.

Basis risk is the Achilles' heel of parametric insurance. Regardless of its scalability, insurance becomes futile if it cannot be relied upon. Basis risk emerges when the parameters triggering insurance payouts do not perfectly align with the actual losses suffered. Consequently, policyholders may not receive compensation even when facing real damages.

The Missing Middle

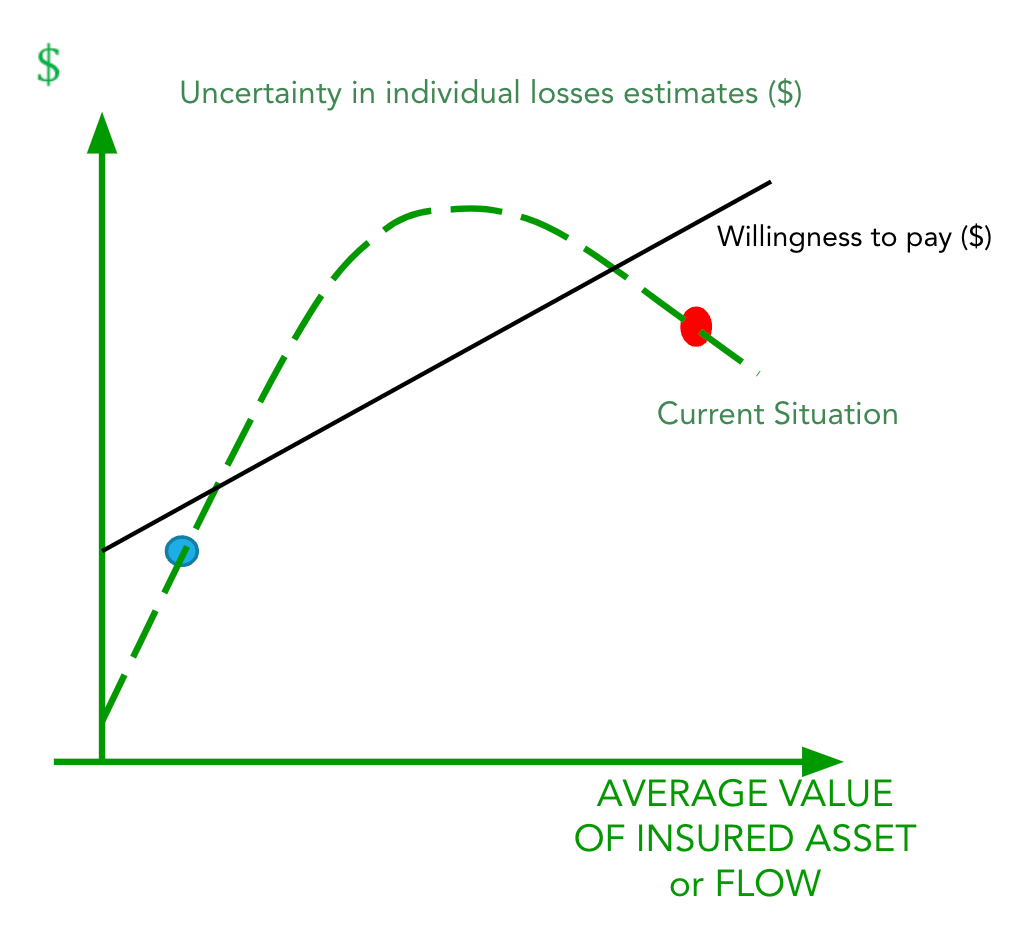

Despite the challenge of basis risk, parametric insurance can still add substantial value, particularly at the lower and higher ends of the willingness to pay spectrum. This is exemplified in Figure 1, that plots the relation between willingness to pay and the costs associated with basis risk.

On the lower end of the distribution of asset value basis risk is a cost that can be kept under control, especially compared to the additional value provided by insurance. How can this be the case? Well, individuals and organizations are naturally risk averse, and the aversion to risk is maximized at low levels of income. Think about the difference between a large-scale farm facing a one million dollar loss compared to a small family run farm. The large-scale farm might make up for the losses with its own savings or credit lines. To the small farm, it is a life or death situation where insurance is essential.

Companies like Apollo and Pula exemplify this by offering affordable microinsurance to agricultural production in Africa. Pula serves 1.7M million smallholder farms of 0.6 acres or less in ten African countries and India. Based in Nairobi, Kenya, they partner with government agencies and loan providers to cover the cost of the insurance, which is included in the price of seed and fertilizer, and there is no direct charge to the farmer. Among the coverages Pula provides is weather index insurance to cover failures of seed germination, using satellite data to determine whether there has been sufficient rainfall.

While these solutions may expose insurers to basis risk, they are sufficiently affordable so that the societal value they provide surpasses the associated uncertainties. The average annual insurance premium per farmer of Pula is about $3 to $5.

On the high end of the willingness to pay spectrum, precision can be achieved through investments in advanced technology and data. As a result, the basis risk curve can be bent below the willingness to pay curve and a sustainable product can make it to the market. Descartes, for instance, specializes in providing hail insurance for car dealerships in the US—a costly product that demands precision. Kettle, another innovative parametric insurance company, provides homeowners protection against wildfires. This showcases that, with a higher price point, investing in better technology is economically viable, ensuring a more accurate alignment of payouts with actual losses.

However, a significant gap exists in the middle of the willingness to pay distribution. This segment is underserved, and addressing it is crucial for the widespread adoption of parametric insurance. Catering to the middle market requires innovative approaches to mitigate basis risk without compromising affordability.

The Belly of the Beast

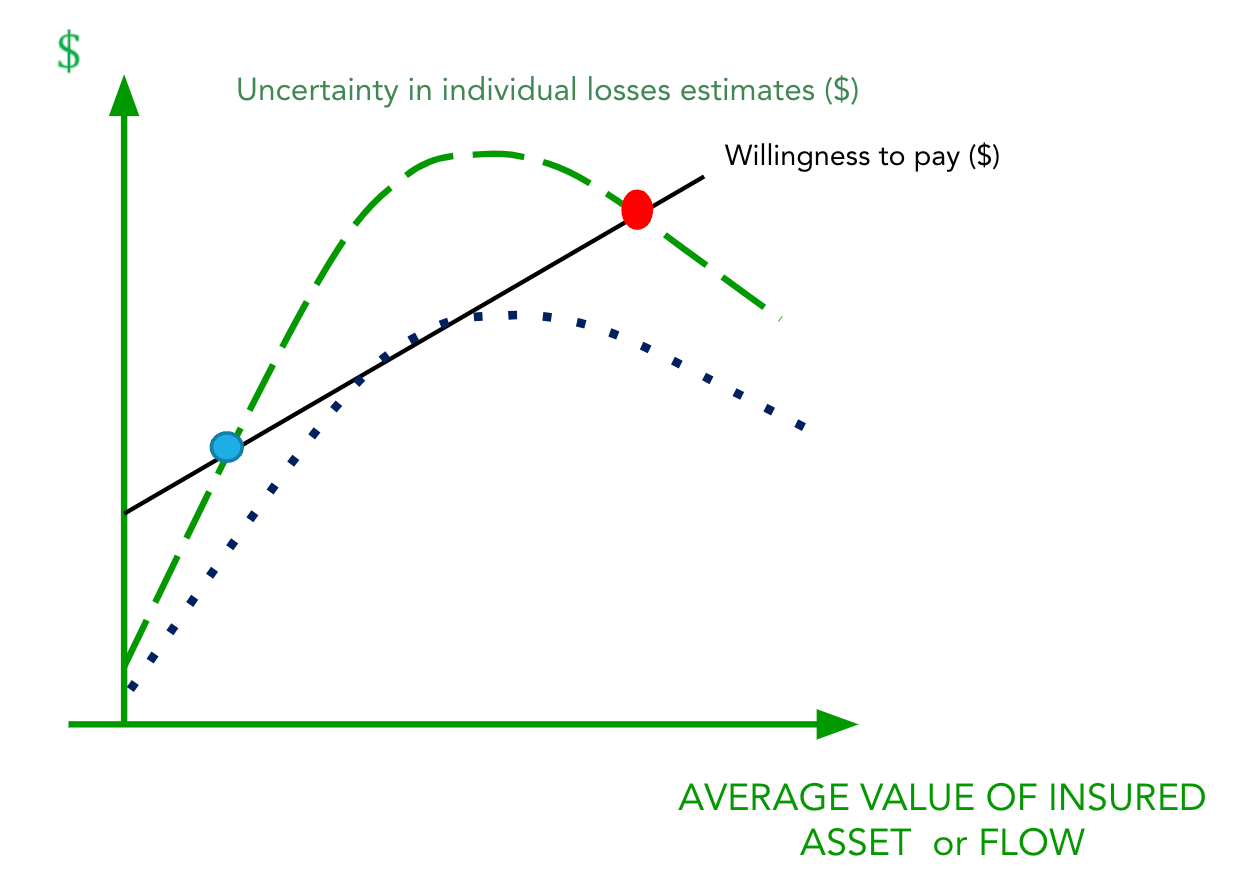

To address the missing middle, it is imperative to solve the basis risk problem. This involves leveraging better data, sophisticated algorithms, and adopting a hybrid payout model that eliminates basis risk. Companies that successfully navigate this challenge can tap into the vast market potential of the middle segment, enhancing the overall attractiveness of parametric solutions. This is exemplified in Figure 2.

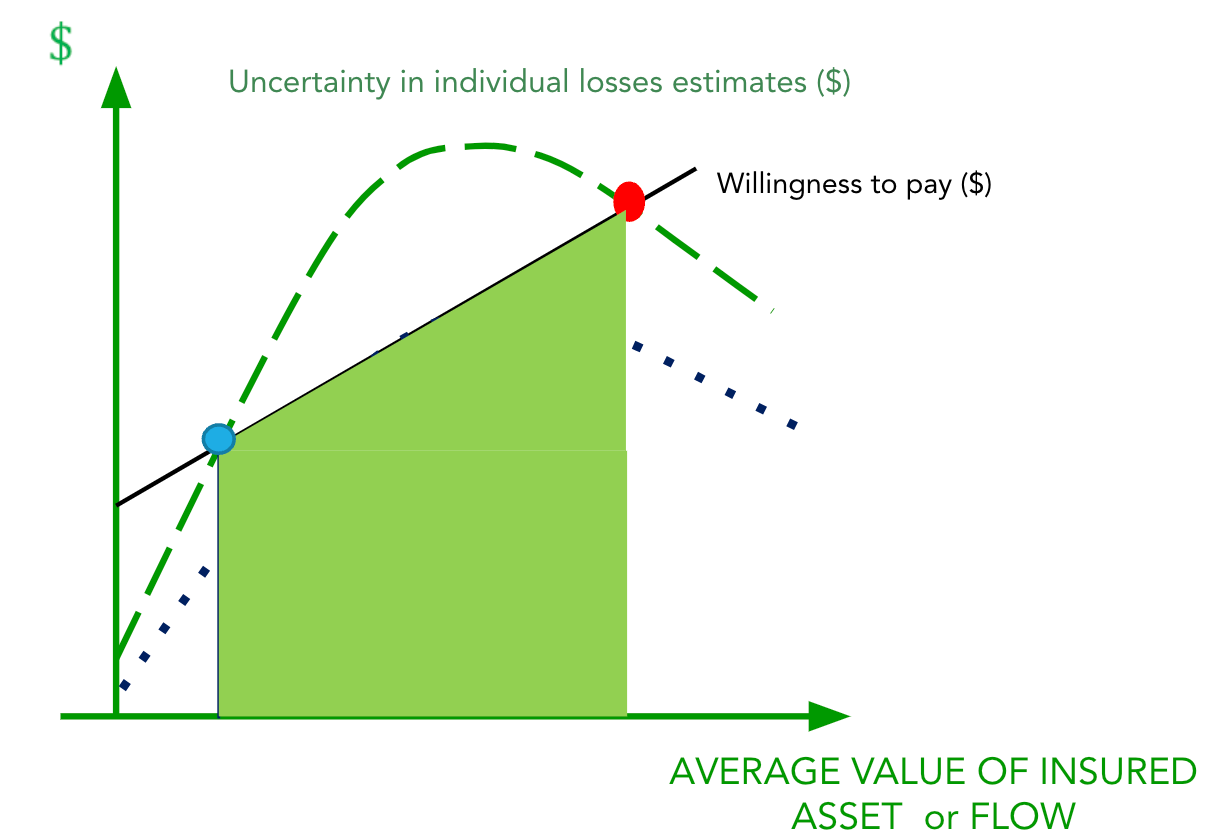

By solving the basis risk challenge and expanding the market, parametric insurance can achieve sustainable long-term success. Growth in the market not only benefits insurers but also provides the scale necessary for reinsurance companies to diversify their portfolios. This diversification, in turn, enhances the overall resilience of the insurance industry, creating a sustainable business model that can withstand the evolving challenges posed by climate change. In Figure 3 we depict the gains from catering to this segment of the market.

The Future

Parametric insurance represents a crucial tool in addressing the impacts of climate change, offering scalability and affordability. However, the basis risk dilemma hampers its reliability. Bridging the missing middle gap by solving the basis risk challenge through better data, algorithms, and hybrid models is essential for unlocking the full potential of parametric solutions. By expanding the market, reinsurers will have more availability to diversify their portfolios. This not only ensures the viability of parametric insurance in the long run but also contributes to the resilience of the broader insurance industry in the face of a changing climate.